Futarchy and Governance: Prediction Markets Meet DAOs on Solana

An Introduction to Futarchy

Traditional governance is failing us. We are in a dark age of ideas, wrought with pessimism, thinking that the solutions we come up with are meaningless — our current world order is the best we have, the culmination of human development, and that’s good enough. Yet, amidst all this disillusionment, a beacon of innovation shines brightly, offering up a radical approach to governance: Futarchy. Albeit experimental, it shows promise, thanks to the Meta-DAO — the first application of Futarchy in practice.

This article covers everything you need to know about Futarchy and the Meta-DAO. The intention is to provide readers with a lucid understanding of Futarchy, how it works, and how they can participate in the Meta-DAO.

Context is provided whenever necessary to ensure any interested reader can understand this article. Despite its overall comprehensiveness, each section is concise in its scope — complex topics are broken down into smaller, manageable sections, allowing anyone to jump into a specific section and start learning immediately.

As this article navigates the challenges of our current governance models, exploring alternatives such as Futarchy becomes more than an academic exercise — it is a necessary exploration into the future of collective decision-making. We are at the cusp of a digital revolution, one premised on ideals of accountability, accessibility, transparency, and efficiency. Futarchy builds upon this promised revolution to usher in a new era of governance.

WTFutarchy?

A Brief Analogy

Imagine you and your friends are trying to guess whether it will rain tomorrow. You have two bowls labeled “Yes, it will rain tomorrow” and “No, it won’t rain tomorrow”. Each of you put money into the bowl corresponding to your belief. The amount of money in each bowl indicates how strongly your group believes it will rain tomorrow. This scenario is like a mini-market, where the “price” (i.e., the amount of money) on each side reflects how likely you and your friends believe the event (i.e., rain tomorrow) will happen.

This brief analogy is crucial for understanding Futarchy, which relies on people buying and selling “bets” on various outcomes. The price of these bets changes depending on how many people, and how strongly they believe, the event will happen. At its core, Futarchy leverages the ideas of prediction markets to guide decision-making in governance systems.

Prediction Markets

A prediction market makes outcomes of future events tradable. They are open, exchange-traded markets that commonly take the form of binary options (i.e., markets based on a simple “yes” or “no” proposition). The market price for an outcome reflects the probability of the result, as thought of by the voting, or betting, populace. The main idea is that prediction markets aggregate beliefs over an unknown future outcome. Traders holding different beliefs buy and sell contracts tied to unknown future outcomes for a specific event. The collective market prices of these contracts are the populace’s consolidated expression of belief. That is, what the populace expects the future result of the event will be.

For a prediction market to function effectively, it requires:

- An unambiguous, publicly known event

- Outcomes to cover all possibilities

- A publicly verifiable oracle for event resolution

- Currency (i.e., a collateral token)

Prediction markets thrive on clarity and specificity. The event must be defined to avoid ambiguity about its occurrence or non-occurrence. This clarity ensures that the voting populace can trade based on a shared understanding of what they are betting on. For example, an event such as “Will Oppenheimer win Best Picture at the 96th Academy Awards?” is a straightforward event that has a verifiable resolution.

A prediction market’s possible outcomes must encompass all potential scenarios to resolve the event conclusively. Using our Oppenheimer example, a binary options market makes the most sense — “Yes,” Oppenheimer will win Best Picture, or “No,” Oppenheimer will not win Best Picture.

This event needs to have a publicly verifiable oracle for determining the event’s outcome. In prediction markets, an oracle is a trusted data source used to determine the result of the event being bet on. For our Oppenheimer example, this oracle would be the Academy of Motion Picture Arts and Sciences — the organization giving out the Best Picture award. We could also include the various news agencies and cable companies covering the event as part of a greater public oracle since they will be publicizing the Academy’s decision. For cryptocurrency specifically, consider the event “Will SOL reach a price of $200 by 5 pm on March 31st, 2024?” The market could use a price oracle such as Pyth or Jupiter’s Price API to verify this outcome.

When traders buy and sell contracts tied to the outcomes of specific events, they put up collateral. Collateral refers to an asset a borrower offers to a lender as a form of protection. This ensures the lender can recover some of their losses if the borrower fails to repay. The choice of collateral is crucial for prediction markets — it must be something of value that participants are willing to stake. The collateral must also be relatively stable and not directly influenced by the market’s outcome. For example, it would be very problematic if the event in question was SOL’s price dropping below a certain threshold and the collateral token used was SOL.

So, what’s Futarchy?

Futarchy, as proposed by Dr. Robin Hanson, builds upon the foundational principles of prediction markets to offer a new governance model. This model makes three general assumptions that justify it as an alternative governance system:

- Democracies often fail to aggregate all available information, leading to suboptimal policy decisions

- The distinction between prosperous and struggling nations is clear, suggesting that effective governance significantly impacts national well-being

- Betting markets excel at aggregating information, making them potentially superior mechanisms for informing policy decisions

Futarchy is the application of prediction markets for governance. It reimagines governance by vesting decision-making authority in the market rather than elected officials or the voting populace — the market shall decide. Futarchy assumes that the collective bets of informed participants can offer a more reliable guide to policy efficacy than traditional voting or expert opinion alone. Futarchy operates on the premise that “we vote on values but bet on beliefs.” While a governance system's overarching goals and values are determined through conventional democratic means, the specific policies to achieve these goals are selected by their predicted effectiveness, as determined by prediction markets. This approach is underpinned by the Efficient-Market Hypothesis (EMH), which states asset prices reflect all available information.

We can define Futarchy formally as:

A form of governance where the policies accepted are ones that prediction markets have clearly estimated to have the most positive effect.

How Does It Work?

At a high level, there are three general stages in a futarchic governance system:

- Values Formation

- Information Sharing

- Policy Recommendation

Values Formation

The process begins with participants collectively deciding on success metrics (e.g., GDP growth, environmental sustainability, public health indicators, national welfare) through traditional methods of democratic participation. This could include direct voting, public forums, or online platforms. This stage ensures that policies align with the community’s priorities.

Community members then create and publish policy proposals targeting these metrics, each with a defined maturity duration for evaluating policy impact.

Information Sharing

Two prediction markets are created for each proposal: one for “Yes” (the policy will be successful) and one for “No” (the policy won’t be successful). Participants provide collateral for tokens representing these outcomes and are incentivized to trade these collateral tokens due to the potential for profit from making accurate predictions. As participants trade on these markets, they contribute to the collective intelligence’s view on the policy’s potential impact.

These markets operate on zero-supply assets, meaning the assets only exist due to trading activity in the market. This allows for participants to buy or sell assets based solely on their predictions. The use of zero-supply assets facilitates a flexible market environment. This type of environment is crucial in reflecting the collective intelligence of the voting populace and their consensus on specific policy outcomes.

Policy Recommendation

After the trading period, the policy with the higher market confidence (i.e., the higher price) is implemented. This step directly translates the collective intelligence of the market into an actionable governance decision. Trades in the losing market are reverted, safeguarding participant’s collateral while encouraging participation. The policy’s success is then evaluated against the initial metrics to assess the accuracy of the market’s predictions. This ensures that implemented policies are not only reflective of community values but are also grounded in empirical evidence of their potential success. Participants in the winning market are rewarded, fostering informed and active engagement in the entire process.

Example

Consider a futarchic government deliberating on a policy to reduce carbon emissions. A speculative market is established to assess the policy’s impact on national welfare, including several metrics on environmental sustainability. Participants trade based on their predictions of the policy’s effectiveness. If the market clearly estimates a significant positive impact, the government would then enact the policy as law, ultimately guided by the collective intelligence of its citizens.

Advantages of Futarchy

Collective Action is an Unsolved Problem

The challenge of collective action is as old as society itself. Epitomized by the tragedy of the commons, this dilemma reveals an unresolved societal question: how can we harmonize individual action with the collective good? This dilemma transcends its traditional application in environmental issues and resource depletion to every level of human cooperation. Past attempts to address the challenge of collective action — through cultural norms, religious teachings, philosophical ideals, and centralized governance — have shown their limitations.

Cultural and religious practices have long bound communities together, promoting altruistic behaviors that align with collective well-being. For example, principles such as the Golden Rule and teachings such as the importance of community and the pursuit of the happiness and virtue of all citizens as the highest good appeared to provide a robust framework for cooperative behavior. Yet, cultural and religious systems often become rigid, slow to adapt to new challenges, and susceptible to exploitation by those who seek personal gain over communal well-being.

Philosophical ideals, such as Plato’s philosopher kings, proposed enlightened leadership as a solution to collective action. Leaders such as Alexander the Great and Marcus Aurelius are said to be examples of this hypothetical concept, possessing enough knowledge to be considered good rulers. However, the rarity of wise and altruistic individuals willing to lead, coupled with the corrupting nature of power, makes this an impractical solution for widespread adoption. We see this play out in modern organizations, which suffer from the principal-agent problem — leaders often take self-serving actions that hurt the group because it is in their interest to do so. For example, the nominations of Prime Minister Boris Johnson for the House of Lords were selected based on their support for his version of Brexit, rather than their ability or service to the public. John Bercow, the previous Speaker of the House of Commons, did not receive a nomination due to his work opposing Johnson.

Modern governance systems attempt to align individual incentives with collective outcomes via democratic processes and corporate governance mechanisms. Despite these efforts, we have yet to solve the issues of information asymmetry, short-termism, and susceptibility to manipulation. These issues often exacerbate the difficulty of making long-term decisions that truly benefit everyone.

These historical approaches have a common theme: while humans possess an innate capacity for cooperation, our methods for organization and making collective decisions are wrought with complexity. In the next section, it becomes evident that traditional methods of governance are struggling to address the nuanced demands of contemporary society. The search for more effective, equitable, and responsive governance systems leads us to consider new paradigms (*cough* Futarchy *cough*) that can better harness collective intelligence for social coordination.

Our Institutions Are Failing Us

Institutions are crucial to a prosperous society. They shape and constrain people’s behavior through their rules and norms. Institutions can be the source of abundance or problems, depending on their strength. For example, Norway is considered one of the best places to live due to its strong institutions. It boasts a high GDP per capita, one of the highest standards of living in the world, an extremely low rate of recidivism, and wide access to secondary and tertiary education.

In contrast, Somalia is an anarchic state characterized by violent crime, weak property rights, and sparse access to basic drinking water. Comparing Norway and Somalia underscores the impact of institutional strength on a country’s prosperity. One could easily conclude that Norway is more prosperous due to the strength of its institutions.

Despite the advantages of strong institutions, there’s growing evidence of their failure in developed countries. The rise of populism and sentiments of anti-establishment in countries such as the United Kingdom, Italy, America, and Canada exemplifies this. For example, if we look at America specifically, trust in American institutions is at an all-time low. In 2022, only 25% of Americans reported confidence in the U.S. Supreme Court. A 2021 study on the 2020 elections shows roughly one-quarter of adults believe that the election was tainted by illegal voting, and 53% of Republicans believe Trump to be the “true president.” The diminishing incentive to research political candidates suggests that the American government is veering towards plutocracy, indicating a failure of traditional governance.

Traditional governance is failing us.

The Solution: Futarchy

In response to these challenges, Futarchy presents a novel approach to governance. It leverages the strength of speculative markets to enhance decision-making and policy effectiveness. Futarchy offers several distinct advantages over traditional modes of governance. Namely,

- Superior Information Aggregation: Prediction markets are exceptional at gathering information. These markets excel at motivating individuals to acquire and share information via trading, culminating in consensus prices that reflect collective wisdom. For example, the market remarkably identified the Morton-Thiokol O-Rings as the underlying cause of the Challenger disaster in 14 minutes, while it took the U.S. government over five months to reach the same conclusion. As a superior instrument for aggregating information, prediction markets can help restore confidence in institutions by implementing better policy under a futarchic governance system.

- Addressing Voter Limitations: Futarchy mitigates issues of voter ignorance and overconfidence by relying on the predictive power of markets. It inherently encourages informed participation, ensuring that only those with credible knowledge will likely influence policy decisions.

- Resistance to Manipulation: Unlike traditional voting systems, where misinformation and emotional appeals can easily sway public opinion, Futarchic prediction markets are more resistant to manipulation. The financial stakes associated with trading create a natural barrier against unfounded speculation as participants are more cautious and deliberate in their decision-making.

- Direct Control by Market Estimates: Futarchy allows market prices to influence policy decisions directly. This ensures that actions are based on the most accurate, up-to-date information. This bypasses traditional governance's often slow and politically motivated decision-making processes, resulting in more timely and effective policy implementation.

- Encouraging Public Participation and Transparency: Futarchy promotes a more engaged and informed citizenry — it involves a broader segment of the population in the decision-making process through market participation. Here, the rationale behind policy decisions is visible and understandable to all, fostering greater trust in governance.

- Flexibility in Policy Approval: Futarchy is ideologically agnostic — “it could result in anything from an extreme socialism to an extreme minarchy,” depending on what the voting populace wants. This allows for a wide range of policy ideas to be considered on their merits, free from political partisanship or ideological bias.

- Enhancing Policy Experimentation and Adaptability: Futarchy’s market-driven approach allows for the quick testing and adaptation of policies. By closely monitoring the market’s reactions to proposed policies, governance systems can become more dynamic to pivot from ineffective measures. This agility in policy experimentation and adaptability ensures governance systems can keep pace with societal and technological advancements, unlike traditional modes of governance.

- Incremental Improvement in Welfare Measures: Futarchy encourages continuous refinement of the metrics used to evaluate policy success, allowing for adjustments and improvements over time. This iterative process ensures that governance evolves in response to the voting populace's changing values and needs.

Futarchy proposes a transformative shift, using the efficiency and intelligence of markets to address the pitfalls of traditional governance and policy implementation. By betting on values but voting on beliefs, Futarchy aims to create a more informed, effective, and responsive governance system that better serves the voting populace’s values and needs.

Criticisms and Limitations

While innovative, Futarchy faces significant criticisms that challenge its feasibility and effectiveness as a governance model. They include:

- Scalability: Futarchy does not inherently scale. While it shows promise for significant, high-stakes decisions (e.g., firing a CEO), its effectiveness for smaller, more routine decisions (e.g., firing a division leader) remains questionable. The concern is that the impact of these less consequential actions may not be adequately reflected in market prices. This could potentially limit Futarchy’s applicability across a broader range of governance decisions.

- Market Manipulation and Power Dynamics: Critics argue that a single powerful entity or coalition could manipulate the market outcomes. This could be done by continuously buying “Yes” tokens and short-selling “No” tokens, swaying prices in their favor. This concern underscores the risk that rich participants would influence policy decisions rather than genuine market consensus. This is amplified by the potential for self-referential market behavior, where participants react to each other’s actions instead of the underlying information. This also raises doubts about Futarchy’s effectiveness at aggregating accurate information.

- Efficient-Market Hypothesis Criticisms: Futarchy’s reliance on the Efficient-Market Hypothesis has been questioned. Investors such as Warren Buffet and George Soros are vocal opponents, disputing the Efficient-Market Hypothesis as a useful theoretical model. The financial crisis of 2007-2008 has also led to renewed scrutiny and criticism. Moreover, empirical evidence has been mixed but has generally not supported strong forms of the Efficient-Market Hypothesis.

- Information Asymmetry: Unequal access to information among market participants could undermine the fairness and effectiveness of Futarchy. Anyone with advanced knowledge or analytical capabilities might disproportionately influence policy outcomes.

- Long-term Forecasting: The long time horizons involved in policy impacts introduce significant uncertainty. Critics argue this makes it difficult for markets to provide accurate forecasts since humans are generally worse at long-range than short-range forecasting. The necessity for markets to be settled — requiring a clear outcome to be determined — complicates the incentive structure, especially when policy effects unfold over decades.

- Budget Constraints and Policy Prioritization: The absence of mechanisms to account for budget constraints and the need for policy prioritization in Futarchy raises questions about its ability to manage finite resources and effectively address competing policy goals simultaneously.

- Simplification of Human Values and Policy Effects: Critics argue that Futarchy’s reliance on a single welfare metric to guide policy decisions drastically oversimplifies the multifaceted nature of human values and the complex impact of different policies. The argument is that reducing governance decisions to market predictions based on a singular metric (i.e., national well-being) could lead to oversights and unintended consequences.

- Vulnerability of Welfare Measures to Corruption and Goodhart’s Law: Selecting official welfare measures that guide policy decisions is complex. These measures must balance robustness against manipulation with the ability to capture nuanced values that genuinely reflect societal well-being. This balance is precarious — introducing detailed proxies for national welfare presents the risk of error and manipulation. In contrast, more objective, harder-to-game proxies can lead to Goodhart’s Law — a measure ceases to be effective once it becomes a target. For example, relying on GDP as a welfare measure could incentivize superficial activities to boost GDP without genuinely enhancing societal welfare.

- Addressing Emergent and Complex Global Challenges: Futarchy remains largely untested. Critics question whether prediction markets can adequately capture the breadth of expertise and consensus needed to tackle emergent and complex global challenges such as climate change.

Addressing these Criticisms

In response to these criticisms, Robin Hanson and other proponents argue that many of them are not unique to Futarchy and can be mitigated with careful design and implementation. Hanson has also directly addressed most of these criticisms in his paper Shall We Vote on Values, But Bet on Beliefs?

For instance, Hanson addresses concerns over market manipulation and power dynamics by highlighting the relative financial power of individual actors versus the collective market. He argues that even the wealthiest of individuals, such as Bill Gates, possess a fraction of the market’s total capital. While someone like Gates could temporarily influence market prices, the broader market will likely correct mispricings if the collective wisdom disagrees with the manipulator’s actions. This self-correcting mechanism is a fundamental strength of Futarchy’s market-based approach.

Futarchy represents a transformative shift in governance, grounded in the belief that markets can enhance decision-making. While criticisms highlight important considerations, Hanson’s counterarguments and the robust framework he proposes suggest a pathway to addressing these concerns.

A key aspect of Hanson’s proposal is experimentation. By starting with smaller-scale experiments and evolving based on the lessons learned, Futarchy could redefine itself to address current criticisms and limitations. Futarchy is not perfect — there is a need for ongoing research and development. The complexities of implementing a market-based governance system are apparent. While theoretical models can provide a strong foundation, real-world applications will reveal these areas for improvement.

Enter the Meta-DAO, the first real-world application of futarchy.

The Meta-DAO: The First Organization Governed by a Market

The Meta-DAO is a new type of organization governed by markets instead of politics. It describes itself as a collective of intellectuals and free-thinkers who aim to reform human coordination by proving futarchy works. It is a protocol built as an ongoing experiment, using the collective intelligence of the market to inform the DAO’s governance and investing decisions. The Meta-DAO is the first organization in the world to employ a futarchical system of governance.

(This is a roundabout way of saying it’s a bunch of terminally online Solana nerds who want to make money by building and investing in the ecosystem while improving it for the better via prediction markets).

For those unfamiliar, a DAO (decentralized autonomous organization) is a member-owned community without centralized leadership. It is managed entirely or partially by smart contracts deployed to a blockchain. Examples of popular DAOs include MakerDAO, ConstitutionDAO, DeveloperDAO, and The DAO. The Meta-DAO falls into this categorization. However, it distinguishes itself by its unique governance model. They argue that Robert Leshner’s Compound Finance governance system has gained widespread adoption. The issue is that Compound Finance’s governance system is only suitable for very simple projects. A Meta-DAO is needed for larger projects — a DAO broken into smaller DAOs tailored to address specific facets of larger projects. We’ll cover this more when we explore how the Meta-DAO works. First, who runs this experimental DAO?

The Futards (fut/acc)

A futard colloquially refers to someone who identifies or associates themselves with futarchy. They can come from all walks of life with varying skill sets. The Meta-DAO relies on a diverse team of futards to maintain and improve the DAO. The core “team” of futards includes notable contributors across various domains:

- Dean and Nico - Spearheading Community Engagement

- Blockchainfixesthis - Leading Content Production

- Proph3t - Overseeing Core Smart Contracts Development and General Operations

- 0xNallok - Overseeing Business Development and General Operations

- Dodecahedr0x - Overseeing the Core Codebase, including UI and Smart Contracts

The “team” is interested in finding more support in the following categories: Social Media, Marketing, Philosophy, Onboarding, Engagement, and Research.

Note, the term “team” is loosely termed due to the decentralized nature of the Meta-DAO. No bosses or corporate hierarchies exist, but leaders are appointed to specific projects. They are not salaried per se but receive compensation for their efforts.

Roles Within the Meta-DAO

Futards can be grouped into one of the following roles:

- Analyst

- Entrepreneur

- Cyber-agent

Analysts are market mavericks — they are strategists, private investigators, and armchair economists. They wield their expertise to navigate the markets and make informed decisions that guide the DAO’s resource allocation. Their analytical prowess allows them to evaluate proposals and opportunities critically. This often leads to lucrative outcomes for themselves as well as the DAO. This is an extremely vital role in a governance system where market dynamics drive decisions.

Entrepreneurs are the catalysts for innovation — they are visionaries who initiate projects that push the boundaries of what’s possible with the Meta-DAO. Entrepreneurs are jacks-of-all-trades. They possess a rare blend of skills — from analytical acumen to sales expertise — to assemble teams, secure funding, and guide their projects to completion. Entrepreneurs are risk-takers, inherently motivated by the potential to create impactful proposals.

Cyber-agents are the backbone of the Meta-DAO. They are the doers — the coders, the designers, and the marketers. Cyber-agents directly translate the DAO’s values and proposals into tangible outcomes. They are versatile, highly skilled in their respective domains, and driven by a commitment to the Meta-DAO’s mission.

The synergy between analysts, entrepreneurs, and cyber-agents is the cornerstone of Meta-DAO’s budding success. So, how exactly do they collaborate? How does the Meta-DAO work?

How Does the Meta-DAO Work?

The Meta-DAO is a practical application of futarchy to manage a collective of profit-seeking entities, which we’ll refer to as members. This expands upon the singular futard and likens them to a sub-DAO, analogous to Helium’s sub-DAOs. Members focus on a single product or service and operate with their own treasury, mirroring the equity structure of a traditional company. These members form the Meta-DAO.

At a high level, the Meta-DAO is structured around the three general steps of a futarchic system — values formation, information sharing, and policy recommendation — but with unique mechanisms tailored to its decentralized nature.

Values Formation: Proposals

Members drive the Meta-DAO’s actions through improvement proposals. These proposals are essentially a set of commands (i.e., Solana instructions) tied to specific members, detailing specific actions to execute if their proposal passes.

For Meta-DAO, the goal “is to make number go up.” Every decision is based on what the market believes is the best outcome for its token, META. Most proposals will include a financial model that breaks down the potential revenue generated using different valuation methods (e.g., VC method, Berkus method, making comparable valuations to similar projects). This information would explain how the member thinks the proposal will affect META's short-, medium-, and long-term value.

Initially, a topic, issue, or initiative is discussed within the Meta-DAO Discord or among external parties. A proposal is then drafted based on one of the following proposal formats:

- Business Project Template

- Business Direct Action Template

- Operations Project Template

- Operations Direct Action Template

Details of the proposal are posted online on a platform such as Medium or HackMD for transparency and accessibility. If enough attention is garnered and the parties responsible for the proposal are sufficiently aligned, the proposal is submitted on-chain.

To submit the proposal on-chain, members must interact with the autocrat program. This is the program that orchestrates futarchy by initializing proposals. A proposal must be initialized with several required fields, including a proposer, description link, and an executable Solana Virtual Machine (SVM) instruction. For example, a member could submit a proposal to transfer 100,000 USDC to a development team’s wallet to create a revenue-generating product managed by the Meta-DAO.

Anyone can submit a proposal.

Information Sharing: Trading Conditional Tokens

Once a proposal is submitted successfully, the autocrat program will initiate the creation of two prediction markets: a conditional-on-pass and a conditional-on-fail market. The pass market represents the expected impact of the proposal, while the fail market represents the status quo. Assuming an efficient market and a sufficiently impactful proposal, the price of META in the pass and fail markets should diverge across the specified trading period. This price difference will inform the Meta-DAO whether the market views a positive expected value from implementing a given proposal.

The astute reader may wonder, “What good is a futarchic system built on a blockchain when we need the ability to revert trades in the losing market?” Blockchains don’t allow users to revert transactions once finalized. So, the Meta-DAO proposes a way to simulate reverting transactions using conditional tokens.

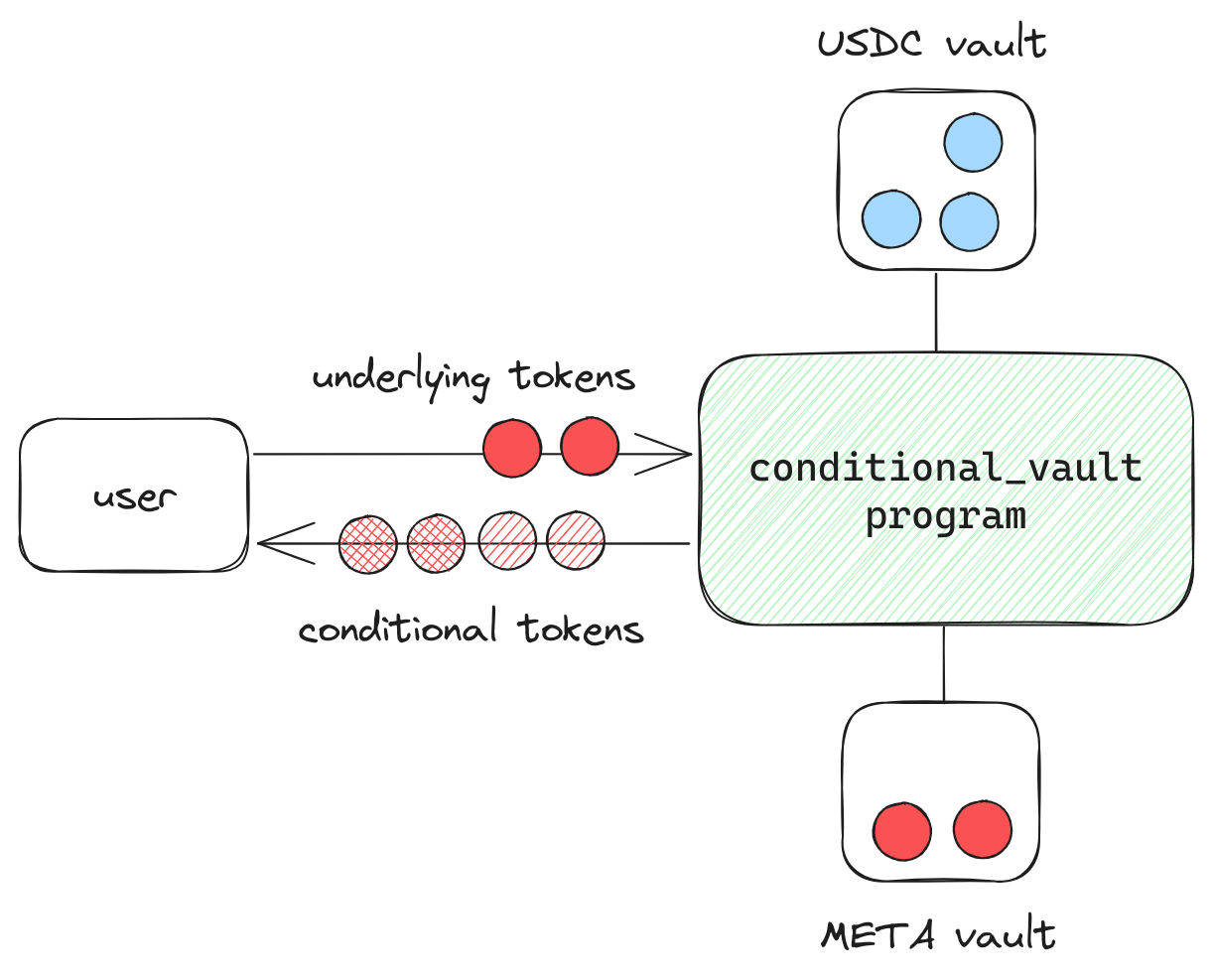

Meta-DAO uses the conditional vault program to facilitate the creation of conditional tokens via conditional vaults. It is a decentralized escrow service that holds funds allocated to the conditional-on-pass and conditional-on-fail markets for a given proposal. These vaults allow the Meta-DAO to simulate reverting transactions. Each conditional vault is associated with a specific underlying token (e.g., META or USDC) and a designated settlement authority, which, in this case, is always the Meta-DAO itself.

Participants can deposit their underlying tokens into these vaults to receive two types of conditional tokens in return: one set that can be redeemed for the original tokens if the proposal is passed (i.e., conditional-on-pass tokens) and another set that can be redeemed if the proposal is reverted (i.e., conditional-on-fail tokens). This system enables participants to speculate on the outcomes of proposals by trading these conditional tokens, allowing them to express nuanced opinions on the proposal’s potential impact on META’s value.

For example, a participant confident in a proposal’s success might deposit 100 USDC into a conditional vault, receiving 100 conditional-on-pass and 100 conditional-on-fail USDC. They could then trade their conditional-on-pass USDC for conditional-on-pass META, securing their position based on their anticipated outcome. If the proposal passes, they can redeem their conditional-on-pass USDC for USDC at the new value based on its success. If the proposal fails, they can redeem their conditional-on-fail META for the original META. This protects the participant’s investment from the proposal’s negative outcome.

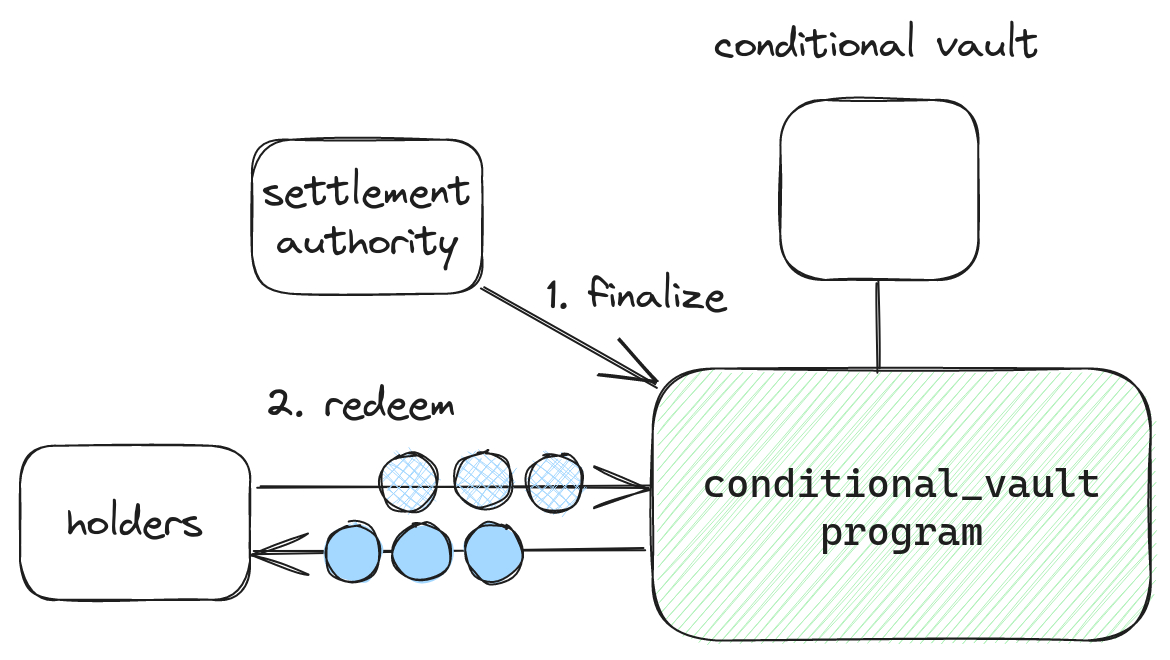

Note that, at any time, the settlement authority (i.e., the Meta-DAO) can finalize or revert a vault.

Time-Weighted Average Price (TWAP) Program

It is important to note that while trading occurs within a proposal’s conditional markets, the price of META in each market is tracked by a time-weighted average price (TWAP) oracle. TWAP is a pricing algorithm used to calculate the average price of an asset over a set period. The Meta-DAO uses a TWAP program to determine the fair market value of the conditional tokens traded within a given conditional market.

All Meta-DAO markets are built using OpenBook V2. However, a TWAP oracle didn’t exist for OpenBook or any other Solana AMM or CLOB. So, they developed their own. The OpenBook TWAP is based on Uniswap V2, meaning:

- There is a running price aggregator for each market

- The current spot price is added to the aggregator before the first trade in a slot. The current spot price is defined as the average of the best bid and the best offer

- One can compute the TWAP between two points using the expression: (current_aggregator - past_aggregator) / slots_elapsed

Using TWAP helps mitigate the impact of short-term price manipulation or volatility. This ensures that the decision-making process is informed by a more stable and representative average price over the trading period. Thus, policy decisions are based on sustained market sentiment rather than temporary fluctuations.

At the end of the trading period, the market with the higher TWAP is finalized, and the action associated with that market is executed.

Policy Recommendation: Resolving a Proposal and Reverting the Failed Market

The finalization process is initiated once the designated trading period, currently set at ten days, has passed. Anyone can trigger a proposal finalization to ensure unnecessary delays don’t hinder the process. The autocrat program then assesses the TWAP of the conditional-on-pass and conditional-on-fail markets. The market with the higher TWAP indicates a collective belief in either the positive impact of the proposal or a preference to maintain the status quo.

If the conditional-on-pass market’s TWAP is >5% of the price of the conditional-on-fail market, the proposal passes. The autocrat executes the related SVM instruction, finalizes the pass market, and reverts the trades made in the conditional-on-fail market. Conversely, suppose the conditional-on-fail market’s TWAP is higher. In that case, the proposal fails, the conditional-on-fail market is finalized, and the trades made in the conditional-on-pass market are reverted to preserve the current state.

Trades in the winning market are realized. This means the conditional tokens are converted into their underlying assets (i.e., USDC or META). This conversion legitimizes the value of the trades in the winning market as they now possess the backing of tangible assets. Conversely, the tokens in the losing market are deemed valueless and are effectively burned as their speculative value does not convert into actual asset backing.

Participants can then redeem their winning conditional tokens for the underlying assets. This completes the cycle of speculation to realization, from trading zero-supply assets in conditional prediction markets to profit. The redemption process is streamlined through the Meta-DAO’s user interface, which we’ll cover in our section How to Participate in the Meta-DAO.

Example Scenario

The Meta-DAO receives a proposal from SolDeFi Innovations for LampRewarder — a novel DeFi application designed to leverage Solana’s low transaction fees and high throughput. LampRewarder aims to reward users with a small amount of lamports for engaging in DeFi activities such as swapping, staking, or providing liquidity for META on specific platforms.

Upon submission, the autocrat program creates two markets: a conditional-on-pass market for approving the development of LampRewarder and a conditional-on-fail market for its rejection. The proposal outlines a clear revenue model for LampRewarder, including transaction fees on rewards, premium features on specific platforms for enhanced user engagement, and revenue-sharing partnerships with other DeFi platforms. This model promises to generate significant revenue for the Meta-DAO’s treasury, improving the value of META.

The trading period sees a surge in support for LampRewarder due to its potential to increase DeFi activity across various DeFi platforms. The community’s enthusiasm is reflected in the rising value of the conditional-on-pass META tokens. Despite some skepticism regarding the sustainability of the project in the long term, the proposal’s detailed revenue model has the majority in support.

After the 10-day trading window, the TWAP for the conditional-on-pass market is significantly higher than that of the conditional-on-fail market. The autocrat program finalizes the conditional-on-pass market, allocating funds from the Meta-DAO treasury to SolDeFi Innovations to develop LampRewarder.

Participants who supported the proposal are rewarded, and the Meta-DAO’s treasury benefits from the new revenue streams generated by LampRewarder.

This scenario underscores the Meta-DAO’s ability to channel the collective intelligence of its members to support initiatives with the potential for impacting community growth, revenue generation, and the appreciation of META.

Meta-DAO: Addressing the Advantages and Limitations of Futarchy

While this sounds promising, how does the Meta-DAO address the previously mentioned criticisms and limitations of futarchy? Doesn’t futarchy fail to scale? Wouldn’t it be susceptible to insider influence and market manipulation? The Meta-DAO’s approach has sparked interest and debate around the practicality and effectiveness of futarchy.

Scalability

One of the most prominent criticisms of Futarchy as a governance model is its lack of scalability, particularly for more minor, routine decisions. However, the Meta-DAO presents a compelling case study in overcoming these criticisms, given its innovative structure and application of futarchic principles. By dividing the organization into smaller, profit-seeking entities, each equipped with its own treasury, the Meta-DAO leverages the composability and efficiency of Solana to create a more scalable and flexible governance model.

Even if the Meta-DAO does run into scalability issues in the future, the adaptability and efficiency of Futarchy could allow the DAO to pivot and adopt other tools and models aimed at improving governance, such as holacracy or liquid democracy.

Market Manipulation and Insider Influence

A common criticism of Futarchy is the potential for market manipulation by wealthy individuals or insiders with disproportionate influence. While Dr. Hanson disputes this with our aforementioned Bill Gates scenario, how does this play out in practice? Proph3t, the founder of the Meta-DAO, should, in traditional respects, have considerable influence over the project he founded. Yet, this isn’t the case. Proposal 3 proposed creating a spot market for META tokens, allowing the broader public to access the token and bootstrap liquidity. Proph3t wasn’t against the general idea. However, he wanted the proposal to fail since he thought it would only benefit the Meta-DAO 5-15%, and the market was mispricing its potential impact at more than twice the current price. Despite being an “insider,” his support for the failure of Proposal 3 did not sway the market.

Similarly, Ben Hawkins created Proposal 6, requesting to mint 1500 META for 50,000 USDC at 33.33 USDC per META. Ben had missed out on the Meta-DAO’s first fundraising round and crafted a proposal he knew would be “spicy,” given the current spot market valuation for META was $55-$60. He committed over $250,000 to drive up the conditional-on-pass market. Despite his influence and wealth, the proposal ultimately failed. In a second time around, Ben tried acquiring 500 META with Proposal 8. Still, his proposal failed.

Pantera Capital, a 4 billion dollar crypto asset manager, proposed to buy $50,000 of META at 100 USDC per META as “an opportunity to test futarchy’s potential as an improved system for decentralized governance.” And yet, the proposal ultimately failed.

These examples underscore a critical insight into the Meta-DAO’s application of Futarchy: the difficulty of manipulating markets when the collective intelligence and speculative power of the community are aligned against such attempts. The Meta-DAO’s use of TWAPs and conditional tokens helps ensure that a stable and representative market consensus informs decision-making. Thus, these instances reflect the Meta-DAO’s steadfast adherence to the principle that the merit of a proposal, as judged by the collective intelligence of the market, outweighs individual influence.

Addressing Thin Markets and Volatility

Concerns regarding the impact of thin markets on policy decisions are mitigated by the nature of prediction markets within the Meta-DAO. Markets influencing significant policies attract interest and participation, thickening the order books over time due to increased speculative trading. This dynamic ensures markets remain robust against manipulation, as evidenced by the previous section.

Moreover, Durden has proposed increasing META’s liquidity via a Dutch auction. Given META's current low volume and high volatility, he argues there is little incentive to provide liquidity. The proposed solution is to implement an auction for the next proposal that begins with a high price, which lowers over time. The goal is to significantly increase the Meta-DAO’s protocol-owned liquidity while moving existing liquidity to a more efficient fee tier, addressing recent complaints and concerns regarding META’s liquidity. Only time will tell how this plays out as the proposal is ongoing; however, it currently looks promising for the conditional-on-pass market.

Current Limitations

Despite these advantages, the Meta-DAO isn’t perfect. Addressing its imperfections requires a technical, strategic response and increased community engagement and participation.

Market Sentiment and Behavior

One observed phenomenon is the tendency for markets predicted to fail to become nihilistic and noisy — due to a combination of rational apathy, moral hazard, and loss aversion. Participants in these markets anticipate a loss and may engage in behavior that distorts the market’s signal quality. This noise can detract from the Meta-DAO’s goal of leveraging the collective intelligence of the markets in decision-making, highlighting the need for future mechanisms that maintain market integrity even in the face of likely defeat.

TWAPs

Another area for improvement is the overreliance on TWAPs to determine market outcomes. While it mitigates short-term price manipulation effectively, a TWAP may not fully capture the nuances of market sentiment or the immediate impact of new information. Exploring alternatives to TWAP could provide more responsive and accurate market signals, reflecting the dynamic nature of the Meta-DAO’s decision-making structure.

Lack of Incentives for Successful Proposals

A notable limitation is the absence of direct incentives for individuals who propose successful proposals. This oversight could dampen the enthusiasm for contributing, as proposers do not receive any tangible rewards for their efforts (unless they ask for some sort of budget that goes back to themselves). Addressing this current pitfall by introducing incentives for successful proposals is crucial. Not only would it motivate more active and thoughtful participation, but it would also ensure the sustained dynamism and innovation that the Meta-DAO aims to foster. Implementing a rewards or recognition system could significantly enhance the quality of proposals, aligning individual motivations with the collective good of the DAO.

Implementing Anti-Frontrunning Measures

The Meta-DAO currently forces the proposer to burn some Lamports as an anti-spam measure. However, checks need to be put in place to see whether the actual Lamport burn is greater than the expected Lamport burn. Implementing such measures can help enhance the fairness and integrity of the DAO’s decision-making process.

Recognizing these limitations highlights the importance of community involvement in refining and advancing the Meta-DAO’s governance model — it’s built by futards, for futards. Each futard holds the potential to contribute to the DAO’s evolution, whether by proposing enhancements, participating in discussions, or trading conditional markets.

As we look to mitigate these limitations, the active participation of every member becomes crucial. Participating in the Meta-DAO is pivotal in shaping a more robust, inclusive, and effective DAO. So, how can you participate?

How to Participate in the Meta-DAO

Join the Discord

The heart of the Meta-DAO beats in its Discord. This is where futards announce updates, draft proposals, and engage in vibrant discussions. If you’re serious about participating in the Meta-DAO, join the Discord. Here, you’ll find a community of futards eager to welcome and discuss new perspectives and ideas. The insights gained, and the connections made with fellow futards will be invaluable.

Contribute

The Meta-DAO is a living, evolving entity. Its growth is fueled by the contributions of its members.

Become a cyber-agent — explore the Meta-DAO’s codebase, see what areas can be improved, and submit a pull request. If you’re not a developer, don’t fret — you don’t have to contribute code. Instead, you could offer an informative Twitter thread, cool UX/UI ideas, marketing for a specific project, etc. The Meta-DAO is incentivized to compensate you for your efforts, whatever they may be, if it provides value to the DAO.

Create a Proposal

Anyone can submit a proposal. First, draft the proposal in the Meta-DAO Discord’s proposal-drafting channel using one of the following templates:

- Business Project Template

- Business Direct Action Template

- Operations Project Template

- Operations Direct Action Template

Proposals can also be drafted externally using one of the templates above — it’s not mandatory to prepare within the Discord. However, getting feedback and garnering interest from your fellow futards is nice.

Then, navigate to https://app.themetadao.org/ and create the proposal, following each step as outlined in the UI:

Trade in Conditional Markets

Participating in conditional markets is crucial for the Meta-DAO’s success. Your trades reflect your beliefs about the potential impact of proposals on the DAO’s future, directly influencing which initiatives are funded and pursued. This mechanism leverages the collective intelligence of the market, aggregating diverse opinions and insights into actional governance decisions. Here’s how you can engage in this process and what to consider while trading:

Get META

There are several ways to obtain META:

- Place a buy order on the Openbook V2 Market via Prism.

- Place a buy order on Birdeye.

- Swap on Jupiter for META.

Ensure you are interacting with the correct token address — METADDFL6wWMWEoKTFJwcThTbUmtarRJZjRpzUvkxhr. Don’t just take my word for it; verify it here.

Start Trading

To trade in conditional markets, navigate to https://app.themetadao.org/. Click on the latest proposal (i.e., Proposal 10). This will navigate you to the following page:

Mint conditional tokens via the modal on the left (this will require a META or USDC balance, depending on what you have selected):

.png)

In the screenshot above, we’re minting 100 pMETA (for trading in the conditional-on-pass market) and 100 fMETA (for trading in the conditional-on-fail market). Use these conditional tokens to trade in the pass and fail markets, depending on your beliefs regarding the given proposal:

OpenBook uses a crank mechanism for its order accounts to ensure they’re up-to-date. Cranking involves processing events to reflect the latest state of orders, which is essential for maintaining market accuracy and efficiency:

Once the trading period is over, all remaining orders can be closed, and tokens can be redeemed using the modal on the left:

What to Consider While Trading

Evaluate the proposal’s value. Your primary role as a trader is to assess whether a given proposal will add value to the Meta-DAO. This evaluation is reflected in the price movements of META. Ask yourself: How does the proposal’s potential impact the DAO’s goals and objectives? How does this align with your understanding of value creation within the ecosystem?

Evaluate the market price. Analyze whether the current price of META accurately reflects your believed value of the Meta-DAO. If you believe META is undervalued, buying META could be a strategic move. Conversely, if META is overpriced, selling could reflect your caution or skepticism on the Meta-DAO’s current trajectory. This also applies to evaluating the conditional-on-pass and conditional-on-fail markets regarding the proposal’s potential impact.

Evaluate your reasoning and motivations for trading. Understand why you’re motivated to trade and how this aligns with the broader market consensus. Are you driven by technical analysis, fundamental valuation, or speculative trends? Recognizing the diversity of thought and strategy among participants can help you navigate the market more efficiently.

Evaluate the aggregation of market pressure. Remember, the market price of META is the result of collective buying and selling pressures. Your participation contributes directly to this dynamic, influencing the equilibrium price. Engage in the market with an informed perspective to steer the Meta-DAO towards decisions you believe are in its best interests.

Evaluate your time horizons. Consider the temporal implications of your trading strategy. Are you trading based on immediate reactions to proposals, or are you considering the Meta-DAO’s long-term potential? Balance short-term tactical trades with a long-term strategic outlook to enhance your contributions to the Meta-DAO’s governance and inherent value.

Final Thoughts

The current world order presents itself as the natural progression of history and the true culmination of human development. With the collapse of the Soviet Union, the only “real” example of a non-functional capitalist society in recent times, liberal democracy’s version of capitalism appears to be the only way forward. Scholars such as Francis Fukuyama argued that the end of the Cold War market was the “end of history” in a Hegelian sense, and Samuel P. Huntington argued that the age of ideology had ended.

This worldview is seen as the primary mode of function, regardless of whether people realize its flaws or externalities. This world order has a reflexive impotence — people realize how flawed our current governance systems are. However, they take a doomerist stance, believing nothing can be done to change it. Even anti-establishment actions or sentiments reinforce this worldview, offering a temporary catharsis that doesn’t challenge our current governance systems in any meaningful way.

By examining the growing trend of political disillusionment in developed countries such as America, it becomes apparent that traditional governance is failing us. Our current modes of governance are slow, inefficient, and filled with cronies acting within their own self-interest.

Is this it? Can we do better?

Futarchy promises a compelling way forward to revamp our current modes of governance. It leverages the collective intelligence and efficiency of prediction markets to streamline meaningful policy implementation that targets metrics of collective well-being. It presents a model that addresses the failures of democracy to aggregate information, efficiently implement policy proposals, work towards collective well-being, and develop an informed citizenry that’s actually interested in governance.

Of course, futarchy is not without its flaws. Yet, the Meta-DAO directly addresses these criticisms as the first application of futarchy in governance. Albeit experimental, it leverages a decentralized organizational structure and prediction markets to create an organization to improve the Solana ecosystem and appreciate the DAO’s inherent value.

Meta-DAO is an experiment and a compelling one at that. Economists have a growing consensus that institutions play a significant role in societal well-being. Developing a new institution that is better than the existing ones is challenging. But, if you can come up with one, there’s a possibility, however small, that it can change the world for the better. Futarchy is one of these possibilities. The Meta-DAO could lay the foundations for a more coordinated and prosperous society. Will it? That’s for the markets to decide.